![]()

[[ type === 'moc' ? 'MARKET ON CLOSE' : 'FREE WEBINAR' ]]

**[[ timeLabel ]]**WATCH LIVE:

Your browser of choice has not been tested for use with Barchart.com. If you have issues, please download one of the browsers listed here.

Join Barchart Premier for advanced OPTIONS screeners and volatility tools. FREE 30 Day Trial

![]()

![]()

Log InMenu

Stocks | Futures | Watchlist | News | More

Advanced search

or

Select a CommodityWheatCornSoybeansSoybean MealSoybean OilOatsRough RiceHard Red Winter WheatSpring WheatCanolaCrude Oil WTIULSD NY HarborGasoline RBOBNatural GasCrude Oil BrentEthanolGoldSilverHigh Grade CopperPlatinumPalladiumAluminumLive CattleFeeder CattleLean HogsPork CutoutClass III MilkNonfat Dry MilkDry WheyButter Cash-SettledCheese Cash-SettledCotton #2Orange JuiceCoffeeSugar #11CocoaLumberS&P 500 E-MiniNasdaq 100 E-MiniDow Futures E-MiniRussell 2000 E-MiniS&P Midcap E-MiniS&P 500 MicroS&P Nasdaq MicroS&P 500 VIXU.S. Dollar IndexBitcoin MicroEther MicroBritish PoundCanadian DollarJapanese YenSwiss FrancEuro FXAustralian DollarMexican PesoNew Zealand DollarSouth African RandBrazilian RealT-BondUltra T-Bond10 Year T-Note5 Year T-Note2 Year T-NoteUltra T-Note30 Day Fed Funds3-Month SOFRCrude Oil BrentCrude Oil WTIGas OilUK Natural GasDutch TTF GasRBOB BlendstockHeating OilEuro BundEuro BoblEuro SchatzEuro BuxlEuro OAT Long-TermEuro BTP Long-TermEurex Conf Long-TermEuro Bono Long-Term10-Year Long Gilt3-Month EuriBor3-Month ESTR3-Month SONIA3-Month SARONRapeseedFeed WheatMilling WheatCornEuro Stoxx 50 IndexFTSE 100 IndexDAX IndexSwiss Market IndexCAC 40 IndexAEX IndexBEL 20PSI 20IBEX 35-MiniOMX Swedish IndexVSTOXX MiniSteel ScrapSteel RebarCocoa #7Coffee Robusta 10-TSugar White #5

Watchlist | Portfolio | Dashboard

MAIN MENU

ETFs Futures Currencies Watchlist

Investing News Tools Portfolio

POPULAR

Stocks Percent Change Top 100 Stocks Stocks Highs/Lows Stocks Volume Leaders Unusual Options Activity Options Volume Leaders

CommoditiesGrainsEnergiesAlertsPre-MarketPost-Market

- Stocks Stocks

Market Pulse

- Stock Market Overview

- Market Momentum

- Market Performance

- Top 100 Stocks

- Today's Price Surprises

- New Highs & Lows

- Economic Overview

- Earnings Within 7 Days

- Earnings & Dividends

- Stock Screener

Barchart Trade Picks

Performance Leaders

Before & After Markets

Most Active

Indices

- Market Indices

- S&P Indices

- S&P Sectors

- Dow Jones Indices

- Nasdaq Indices

- Russell Indices

- Volatility Indices

- Commodities Indices

- US Sectors Indices

- World Indices

Trading Signals

- New Recommendations

- Top Stocks to Own

- Top Signal Strength

- Top Signal Direction

- Stock Signal Upgrades

Sectors

-

Options Options

Market Pulse

Volatility

Volume & Open Interest

- Most Active Options

- Unusual Options Volume

- Options Volume Leaders

- Highest Open Positions

- Change in Open Interest

- %Change in Open Interest

Data & Tools

Option Screeners

Income Strategies

Vertical Spreads

Protection Strategies

Straddle and Strangle

Horizontal Strategies

- Long Call Calendar

- Long Put Calendar

- Long Call Diagonal

- Short Call Diagonal

- Long Put Diagonal

- Short Put Diagonal

Butterfly Strategies

- Long Call Butterfly

- Short Call Butterfly

- Long Put Butterfly

- Short Put Butterfly

- Long Iron Butterfly

- Short Iron Butterfly

Condor Strategies

-

ETFs ETFs

Market Pulse

- ETF Market Overview

- Popular ETFs

- ETF Finder

- Top 100 ETFs

- Today's Price Surprises

- New Highs & Lows

- Top Dividend ETFs

- ETF Screener

Performance Leaders

Before & After Markets

Most Active

Trading Signals

Mutual Funds

Market Pulse

- Futures Market Overview

- Long Term Trends

- Today's Price Surprises

- Highs & Lows

- Futures Market Map

- Performance Leaders

- Most Active Futures

- Prices by Exchange

Commodity Groupings

- Commodities Prices

- Currencies

- Energies

- Financials

- Grains

- Indices

- Livestock

- Metals

- Softs

- Mini & Micro Futures

Futures Trading Guide

Commitment of Traders

Resources

- Contract Specifications

- Futures Expirations

- First Notice Dates

- Options Expirations

- Economic Calendar

Cash Markets

European Futures

- Euro Futures Overview

- Long Term Trends

- Today's Price Surprises

- Highs & Lows

- Futures Market Map

- Performance Leaders

- Most Active Futures

European Groupings

- Commodities Prices

- Energies

- Financials

- Grains

- Indices

- Metals

- Softs

- Europe Power Futures

- Europe Gas Futures

- Baltic Freight Indices

European Trading Guide

Forex Market Pulse

- Forex Market Overview

- Long Term Trends

- Today's Price Surprises

- Highs & Lows

- Forex Market Map

- Performance Leaders

- Currency Converter

Crypto Market Pulse

Trading Signals

Commitment of Traders

Currency Groupings

- Popular Cross Rates

- Australian Dollar

- British Pound

- Canadian Dollar

- Euro FX

- Japanese Yen

- Swiss Franc

- US Dollar

- Metals Rates

- All Forex Markets

Crypto Groupings

Investing Ideas

Insider Trading

Today's Picks

My Screeners

Technical Ideas

- Bullish Moving Averages

- Bearish Moving Averages

- Breakouts and Reversals

- Candlestick Patterns

- eMACD Buy Signals

- Hot Penny Stocks

- RSI Bullish Divergence

- RSI Bearish Divergence

- Short Interest Stocks

- Standout Stocks

- Top Stocks Under $10

- TTM Squeeze

- Up Trending Stocks

- Down Trending Stocks

Dividend Ideas

Power Investors

Themed Lists

-

News News

Barchart

Featured Authors

- Andrew Hecht

- Austin Schroeder

- Caleb Naysmith

- Darin Newsom

- Don Dawson

- Elizabeth Volk

- Gavin McMaster

- Jeannine Mancini

- Jim Van Meerten

- Justin Estes

- Mark Hake

- Oleksandr Pylypenko

- Rich Asplund

- Rick Orford

- Rob Isbitts

- Sarah Holzmann

- All Authors

Commodity News

Financial News

Free Newsletters

- All Free Newsletters

- The Barchart Brief

- Active Investor

- Unusual Options Activity

- Dividend Investor

- Pre-Market Bulletin

- Commodity Bulletin

- Chart of the Day

- Ag Market Commentary

Press Releases

Member Tools

- My Watchlist

- Investor Portfolio

- Standard Portfolio

- Dashboard

- Symbol Notes

- Alert Center

- Alert Templates

- Barchart Screeners

- My Charts

- Custom Views

- Barchart Custom Views

- Chart Templates

- Barchart Chart Templates

- Compare Stocks

- Daily Prices Download

- Historical Data Download

My Custom Reports

- Watchlist Emails

- Standard Portfolio Emails

- Investor Portfolio Emails

- Screener Emails

- End-of-Day My Charts

- End-of-Day Reports

Manage Tools

- Organize Watchlists

- Organize Portfolios

- Organize Investor Portfolios

- Organize Screeners

- Organize My Charts

My Account

Knowledge Base

Barchart Webinars

Barchart Live

Membership

Barchart Resources

- Technical Indicators

- Barchart Trading Signals

- Time & Sales Conditions

- Barchart Special Symbols

- Barchart Data Fields

Options Resources

- Profit & Loss Charts

- Options Volatility

- Options Greeks

- Covered Call

- Naked Put

- Long Call Option

- Deep ITM Calls

- Long Put Option

- Credit Spreads

- Short Straddles

- Short Iron Condor

- 7 Ways to Make Money

- Hedge Stocks with Options

Site News

Market:

-

US

-

Canada

-

UK

-

Australia

-

Europe

News Menu

News

-

Barchart

-

Featured Authors

-

Commodity News

-

Financial News

-

Free Newsletters

-

Press Releases

AI Power Stocks Could Be a Once-in-a-Generation Trade. Start With the Companies Behind Every Data Center.

Rick Orford -Barchart - Fri Jun 26, 5:01PM CDTColumnist

All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here

Share

![]()

![]()

/Renewable%20Energy%20by%20Yuri%20Hoya%20via%20Shutterstock.jpg)

Renewable Energy by Yuri Hoya via Shutterstock

When people think of AI, they usually default to the big names like Nvidia (NVDA), AMD (AMD), Broadcom (AVGO), and Marvell (MRVL). The chip producers, the ones that are reporting double to triple-digit growth quarter over quarter. The ones that dominate headlines with big green charts and arrows every time.

But it takes far more than silicon to run artificial intelligence (AI).

Every AI model, every chatbot response, and every image generation request ultimately runs inside a data center. And those data centers consume staggering amounts of electricity.

In fact, as AI workloads continue to expand, power increasingly becomes the limiting factor in day-to-day operations. You can have the newest and most advanced GPU clusters around, all cooled by the most sophisticated thermal tech in the industry, connected by the best networking platforms in the world.

But none of that matters if you don’t have enough electricity to turn on any of the servers.

That's why some investors are looking beyond semiconductors and toward a less obvious beneficiary of the AI boom: the companies that generate and deliver the power that keeps these data centers online, and the ones that are building the parts that make it all happen.

Why AI is driving a $2.2 trillion power market

The power generation industry is valued at around $1.3 trillion today, according to industry estimates, and is expected to grow to $2.2 trillion by 2034.

Historically, the biggest driver of the power generation industry was the increasing urbanization of developing countries. But the sharp rise in data center demand, with its enormous requirements for computing power, is what’s further driving that expected growth.

As a result, companies across the power value chain stand to benefit from what could become a decade-long investment cycle, not only from AI but also from secular tailwinds.

Where are the sector bottlenecks?

Before anything else, we need to cover where the opportunities are in the power sector, at least in the context of AI demand. And to do that, we need to break down the value chain and see where the bottlenecks lie.

Power producers and the 20-year PPAs feeding AI data centers

First, we have the raw materials and energy producers. Think fuels: natural gas (NGQ26), solar, wind, and uranium, as well as the companies that convert them into energy. This is the business at the very base of the value chain, where everything starts.

Historically, many power producers sold electricity into wholesale markets, where prices fluctuate based on supply and demand. But the rise of AI is changing that dynamic.

Hyperscalers such as Microsoft (MSFT), Amazon (AMZN), Google (GOOGL), and Meta (META) increasingly need guaranteed, 24/7 access to massive amounts of power. By that, I mean they can’t just connect to a light socket and call it a day. They need to go straight to the power producers to get what they need.

Power producers respond, usually in the form of power purchase agreements (PPAs), in which the data center operator commits to buying electricity from a producer for extended periods, often lasting 20 or more years. These agreements provide energy companies with stable, predictable cash flows while giving data center operators confidence that sufficient power will be available as they expand capacity.

So, when you see a power company bagging one of these PPAs from a hyperscaler, you know you’re seeing trust and validation in one deal. Now, if you see multiple deals, well, that just solidifies the bull case.

The biggest example of this kind of relationship is between Microsoft and Constellation Energy.

Constellation Energy ( CEG): The go-to stock for AI nuclear power

CEG has bagged mega Mag 7 deals.

CEG has bagged mega Mag 7 deals.

Just a couple of years ago, Microsoft inked a deal with CEG to create the Crane Clean Energy Center. This is a project that was widely reported to restart Unit 1 of the (former) Three Mile Island nuclear plant. The deal is for 20 years, with the PPA being so big that Constellation is investing ~$1.6 billion to bring the reactor (back) online for Microsoft.

Once Unit 1 is online, it could make as much as 7 million megawatt-hours of power per year, assuming everything runs as planned.

If that’s not all, last year, Meta inked a deal with Constellation to launch the Clinton Clean Energy Center. Like with Microsoft, the deal is for a 20-year PPA, and CEG will add an additional 30 megawatts of output by way of nuclear uprates. This particular PPA covers 1.21 gigawatts of clean nuclear power, which could translate to ~9 million megawatt-hours of annual production.

The Microsoft and Meta deals are standout examples of how CEG can grow for decades. Granted, the exact financial details of the PPAs haven’t been made public, but you can be almost sure they are going to be lucrative. In fact, some analysts estimate Microsoft could be paying between $110-115 per megawatt hour. If that were the case, it would imply as much as $800+ million in annual revenue - on the Microsoft deal alone.

Of course, CEG is not alone in bagging power deals with hyperscalers.

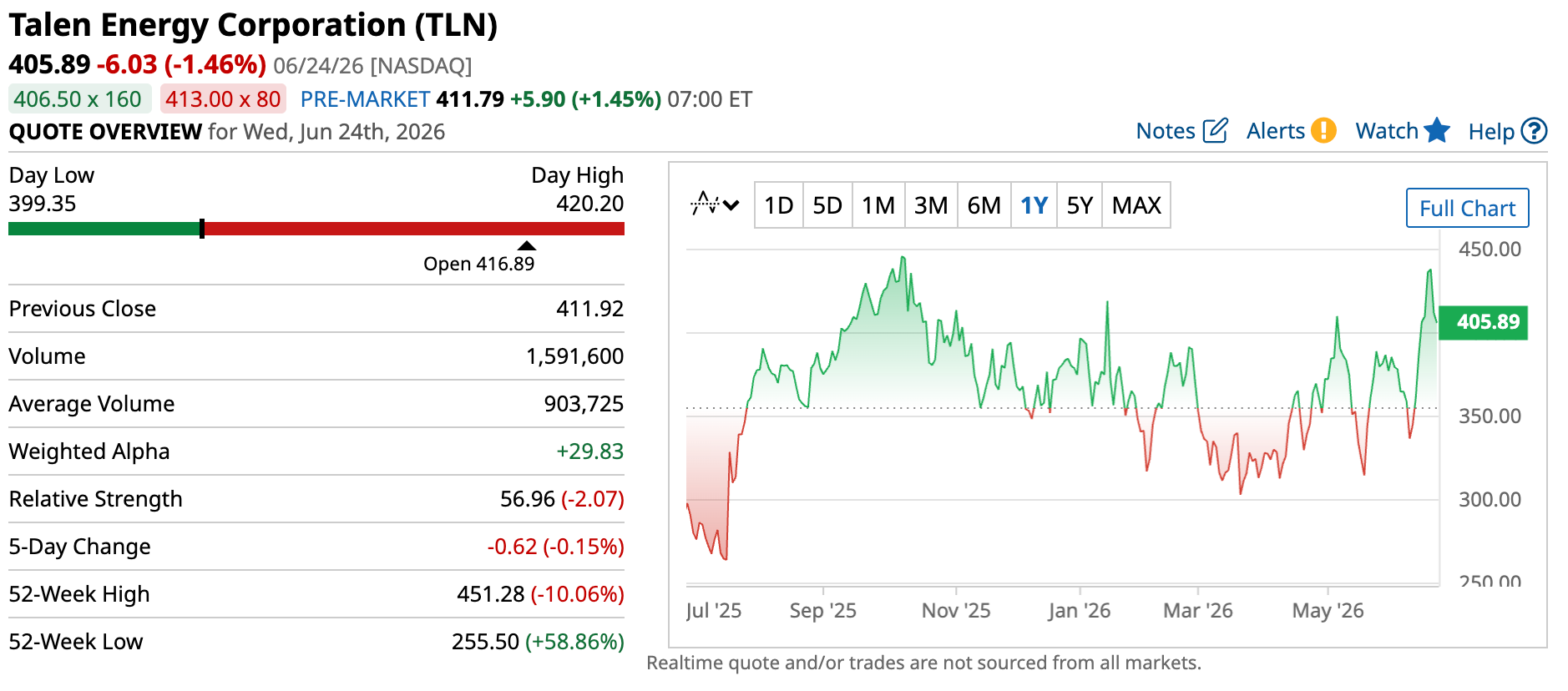

Talen Energy ( TLN): The Amazon nuclear deal next door

Talen linked up with Amazon on a power pact.

Talen linked up with Amazon on a power pact.

Talen Energy, a relatively new player in the space, has partnered with Amazon to produce up to 1.9 gigawatts of nuclear capacity from its Susquehanna plant. But Talen’s plant is directly adjacent to Amazon’s data center.

That means the deal can significantly reduce the need to move electricity across the broader transmission and distribution network. Instead of sending power across hundreds of miles of grid infrastructure, electricity can be delivered almost directly from the source to the data center.

The arrangement not only minimizes transmission losses but also helps hyperscalers secure reliable access to power in a market where grid capacity is increasingly becoming the bottleneck. No congestion pricing, no interconnection delays, and no third-party dependencies to worry about. That’s practically a match made in heaven for data centers.

But, true adjacency – as in building plants right beside data centers, instead of somewhere else that’s relatively nearby – faces growing geographical and regulatory constraints. Even now, just finding “good enough” places to build the next data center is becoming a challenge. Tack on a nuclear plant right beside it? The challenges multiply.

That’s why Talen Energy’s approach, while wildly attractive, may not be the gold standard. And that’s why we need to look into other parts of the value chain.

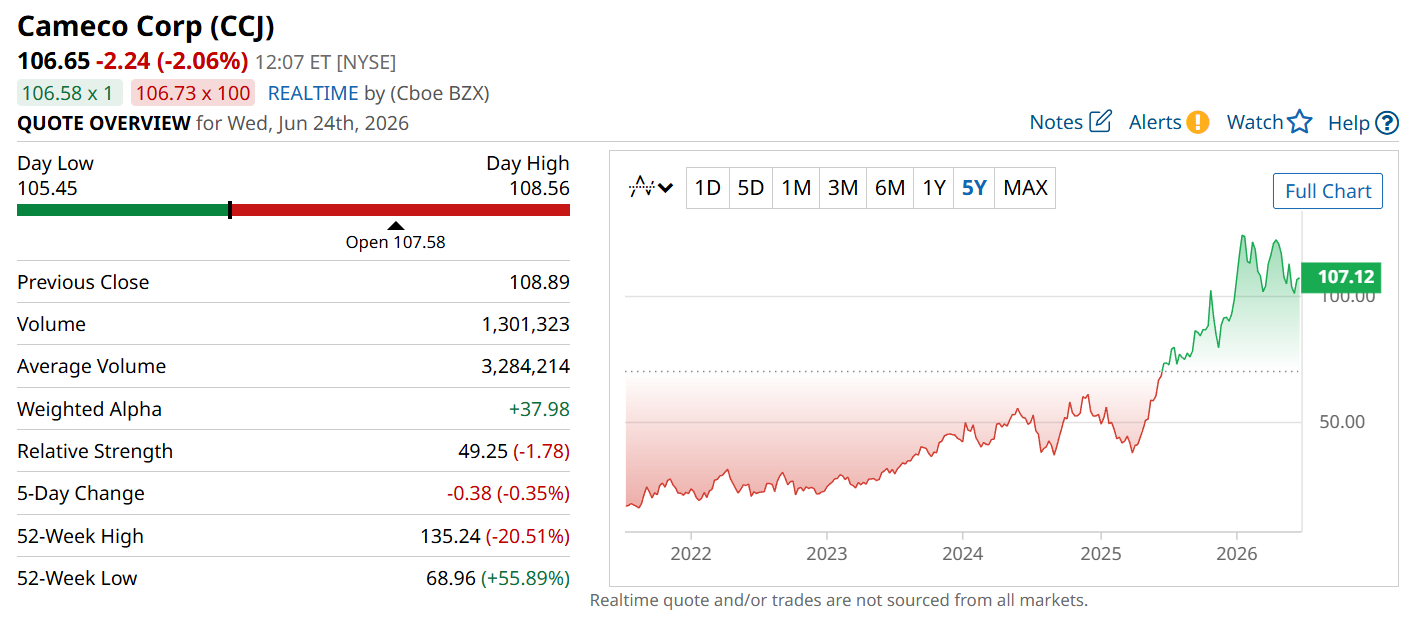

Cameco Corp ( CCJ): The uranium picks-and-shovels play for AI

Now, as for the raw material providers, the relationship is one step removed from hyperscaler deals, but that doesn’t mean they don’t benefit from them. In fact, let me call your attention to another interesting player in the nuclear power space.

CCJ sits further down the value chain.

CCJ sits further down the value chain.

Cameco Corp operates a little further down the value chain. It doesn’t generate electricity, but it does produce uranium oxide concentrate, otherwise known as yellowcake. This is the preferred fuel by many nuclear reactor operators due to its high energy density, reliability, and ability to provide consistent baseload power.

Cameco has major mining operations in Canada and Kazakhstan, and also participates in nuclear fuel services and reactor technology. And while the company’s involvement in AI power growth isn’t as direct as CEG’s, as hyperscalers increasingly lean into nuclear, Cameco should grow. As demand for nuclear energy continues to rise, utilities like Constellation benefit from selling more electricity, while uranium suppliers like Cameco benefit from increased fuel demand. It’s a symbiotic relationship.

Of course, the relationship isn't perfect. Cameco's performance is still heavily influenced by uranium prices, supply dynamics, and long-term contracting activity. But as hyperscalers continue signing nuclear deals and utilities respond by extending the lives of existing reactors or building new capacity, the long-term outlook for uranium demand becomes increasingly attractive.

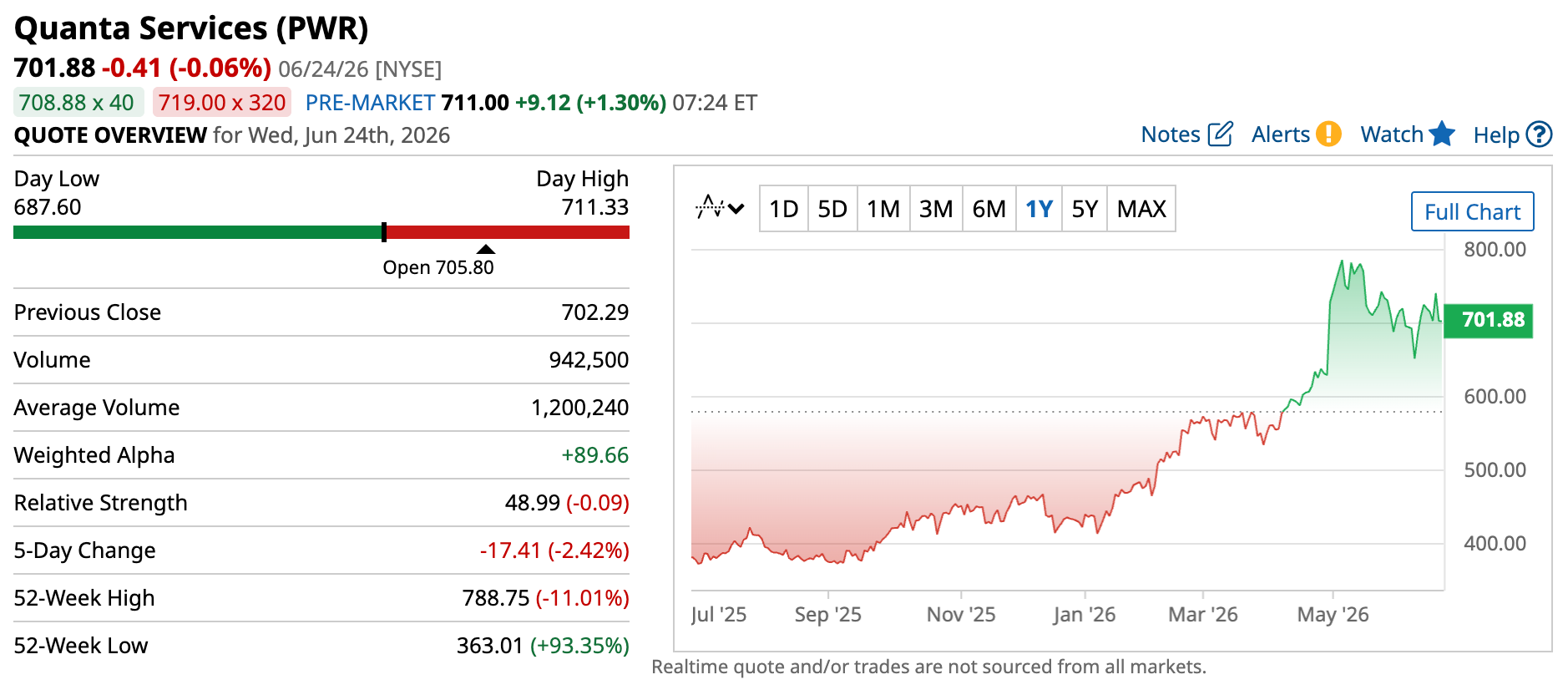

Quanta Services ( PWR): The grid bottleneck behind AI power

Another bottleneck that’s becoming increasingly important for AI power demand is distribution. Transmission lines, substations, and grid infrastructure are all critical to supplying power-hungry data centers. And as one might expect, companies sitting in the crossroads are likely to benefit from the growing demand.

Certain companies that operate with true adjacency, like Talen Energy, remove this requirement entirely. But that’s somewhat unique in the space, so many power providers and hyperscalers still need to deal with distributors.

One of the clearest examples of this is Quanta Services.

Quanta provides the “blood vessels” of the industry.

Quanta provides the “blood vessels” of the industry.

Quanta operates in the physical layer that makes large-scale AI deployment possible in the first place. That includes transmission buildouts, high-voltage substations, and the electrical infrastructure required to connect new data center campuses to increasingly constrained regional grids. It is one of the largest engineering and construction services contractors in North America's power transmission sector.

Think of it this way: energy producers operate the heart, while companies like Quanta make and maintain the blood vessels.

Every new data center, manufacturing facility, or large industrial project still needs to be physically connected to the grid, and they usually opt for the biggest and most capable players. That leaves Quanta well-positioned to capture that demand.

In many cases, the constraint isn’t the generation capacity itself, but the ability to interconnect new load to an already congested transmission system. And that’s where the opportunity is: to take part in data center demand.

Quanta’s management has already highlighted that AI-driven power demand is now a major growth driver for the company. But because of its broader distribution business, demand across other large-load industries also serves as a catalyst.

Now, to be clear, power distribution won’t enter into PPAs. But there is a clear line between increased PPAs from the producers and increased demand for distribution. In fact, if you’ll notice, all four companies I’ve covered so far practically have the same graph over the last five years. Sure, there are small differences in magnitude, but the broader trend is unmistakable: these companies are beneficiaries of the same secular tailwind, practically all at the same time. And it makes sense when you think about it. More AI workloads require more data centers.

More data centers require more electricity, which leads to more power generation, more fuel consumption, and massive investments in transmission and grid infrastructure.

Bottom line: As long as hyperscalers continue their aggressive spending on AI infrastructure, every link in the power production chain stands to benefit.

Electrical equipment stocks: Eaton, Schneider, and GE Vernova

Now, if you thought we were on the ground level, we’re not – at least, not yet. One level deeper are those companies that support both power generation and grid infrastructure. These are the players that actively build, connect, and scale the physical backbone that enables both.

In the broader structure of the AI power stack, this layer sits between high-level grid construction and end-use electricity consumption. It serves as the industrial foundation that determines whether capacity can actually be deployed at speed. In practice, this is where the constraint becomes physical rather than theoretical. Because even if generation capacity is available and even if demand is fully contracted through long-term agreements, none of it translates into usable supply unless the underlying infrastructure can be built fast enough.

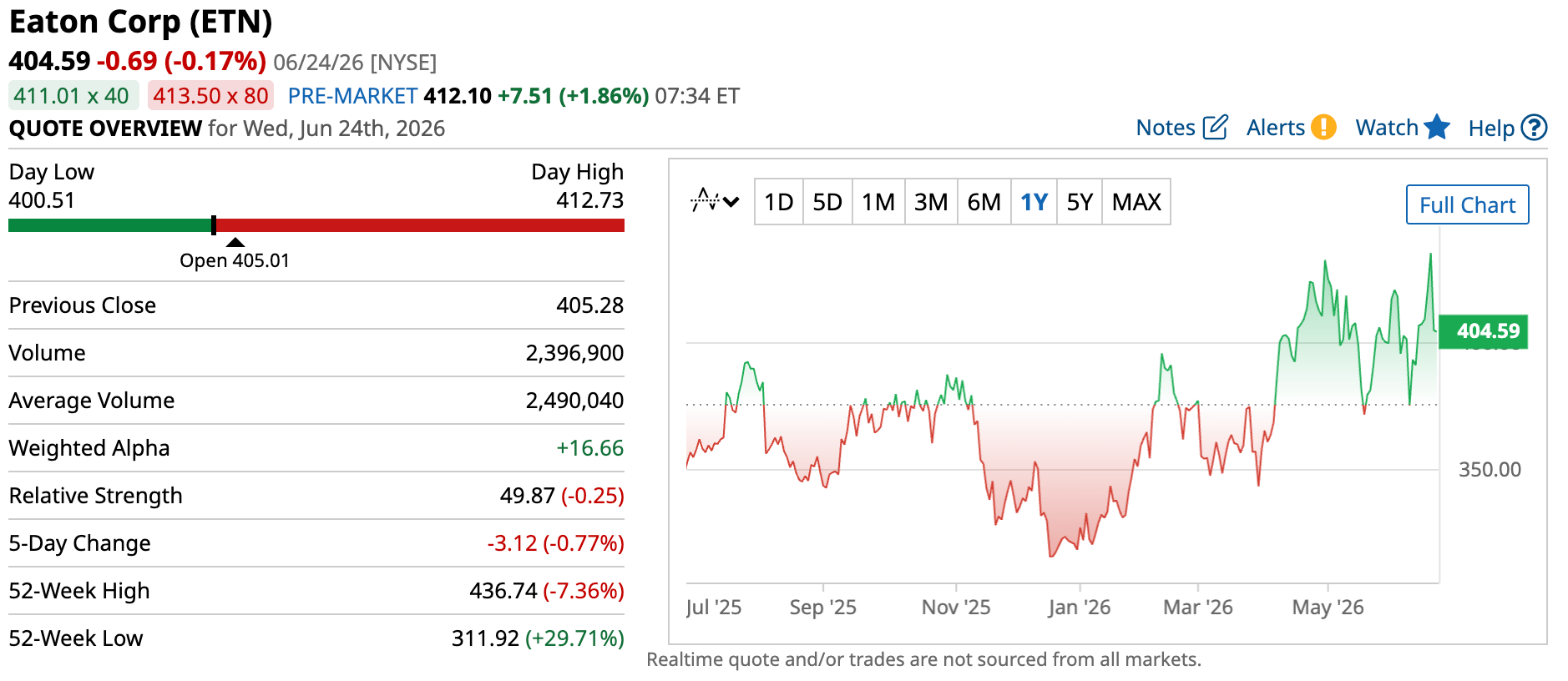

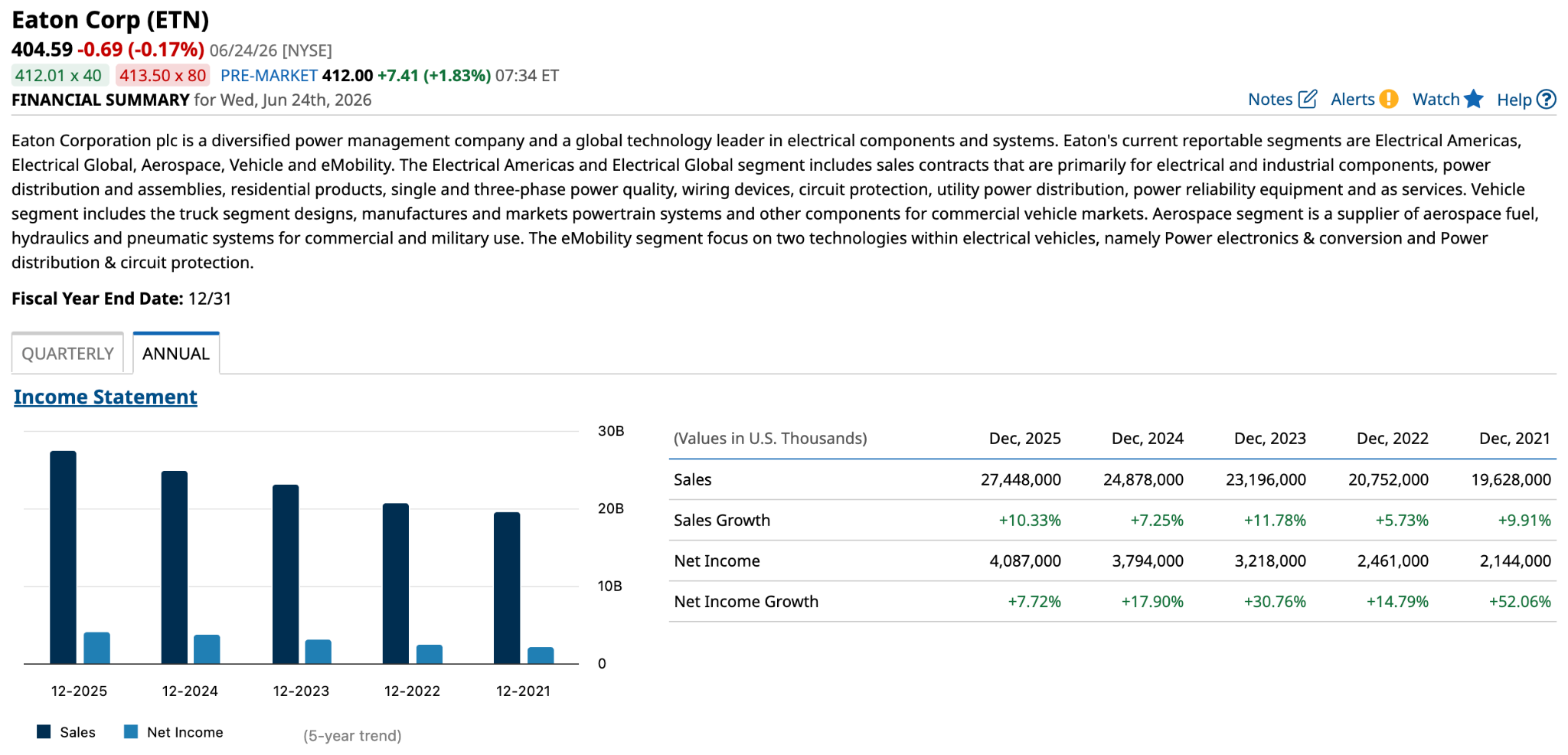

Now we can look to the companies that supply those parts of power production and infrastructure. One good example is Eaton Corp( ETN).

ETN is a clutch equipment pick.

ETN is a clutch equipment pick.

The company manufactures electrical hardware such as switchgear, breakers, transformers, uninterruptible power supply systems, and more. These pieces of equipment are critical components to running not just data centers but also your typical modern industrial enterprise as well.

What makes Eaton particularly relevant today is that these components are not optional upgrades. Electrical systems need these parts. So, we can say increased demand directly translates into increased sales, as a quick snapshot of Eaton’s annual financials will attest.

In effect, Eaton sits in the electrical component layer of the stack, supplying the core hardware that allows both industrial facilities and hyperscale data centers to safely distribute and regulate power at scale.

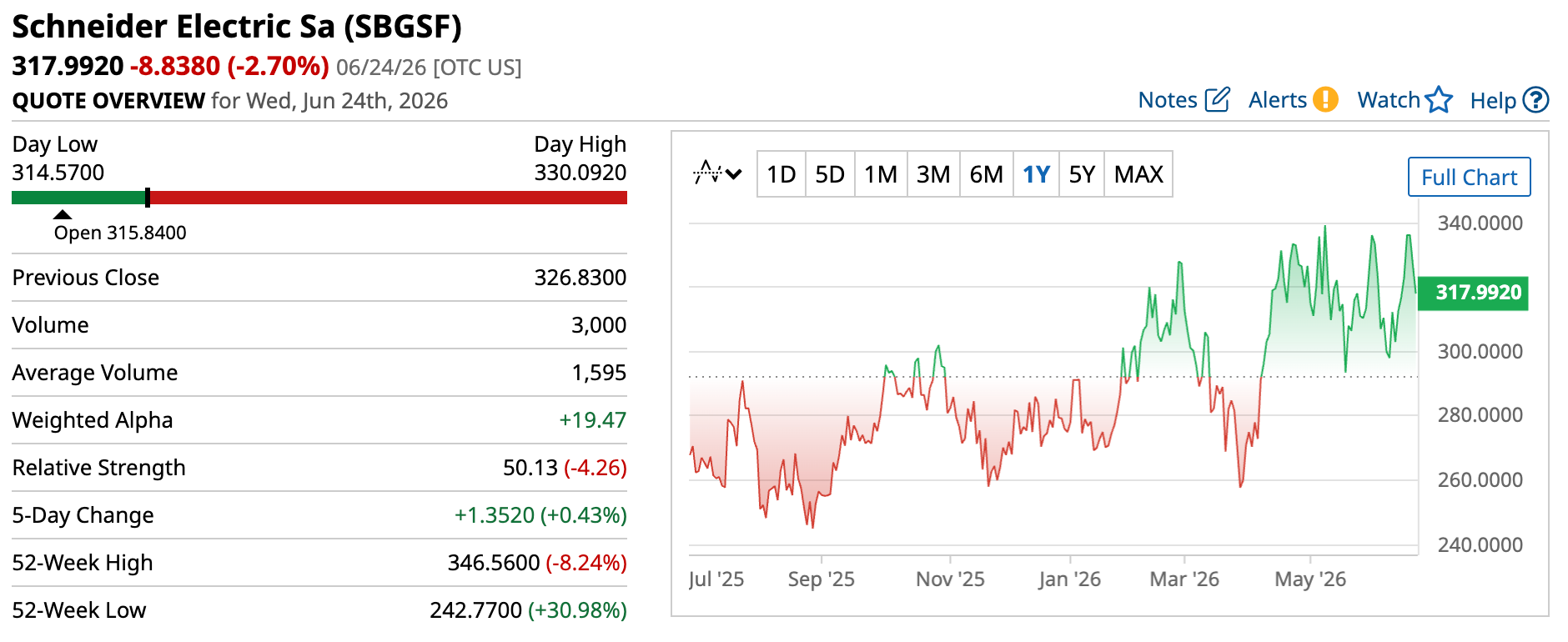

Another, albeit different, example here is Schneider Electric ( SBGSF).

Schneider trades OTC.

Schneider trades OTC.

Unlike component manufacturers, Schneider designs and deploys integrated energy management systems that get deployed in data centers, industrial facilities, and utility networks. The entire value chain.

In practical terms, more and more, Schneider is responsible for how entire facilities manage power flow end to end. Power efficiency matters more in data centers that consume enough electricity to power small cities, where every kilowatt counts and even small, persistent energy losses can translate into massive financial costs.

This positions Schneider closer to the systems and control layer of the grid, where software, monitoring, and integrated electrical architecture determine how efficiently large-scale infrastructure operates once built.

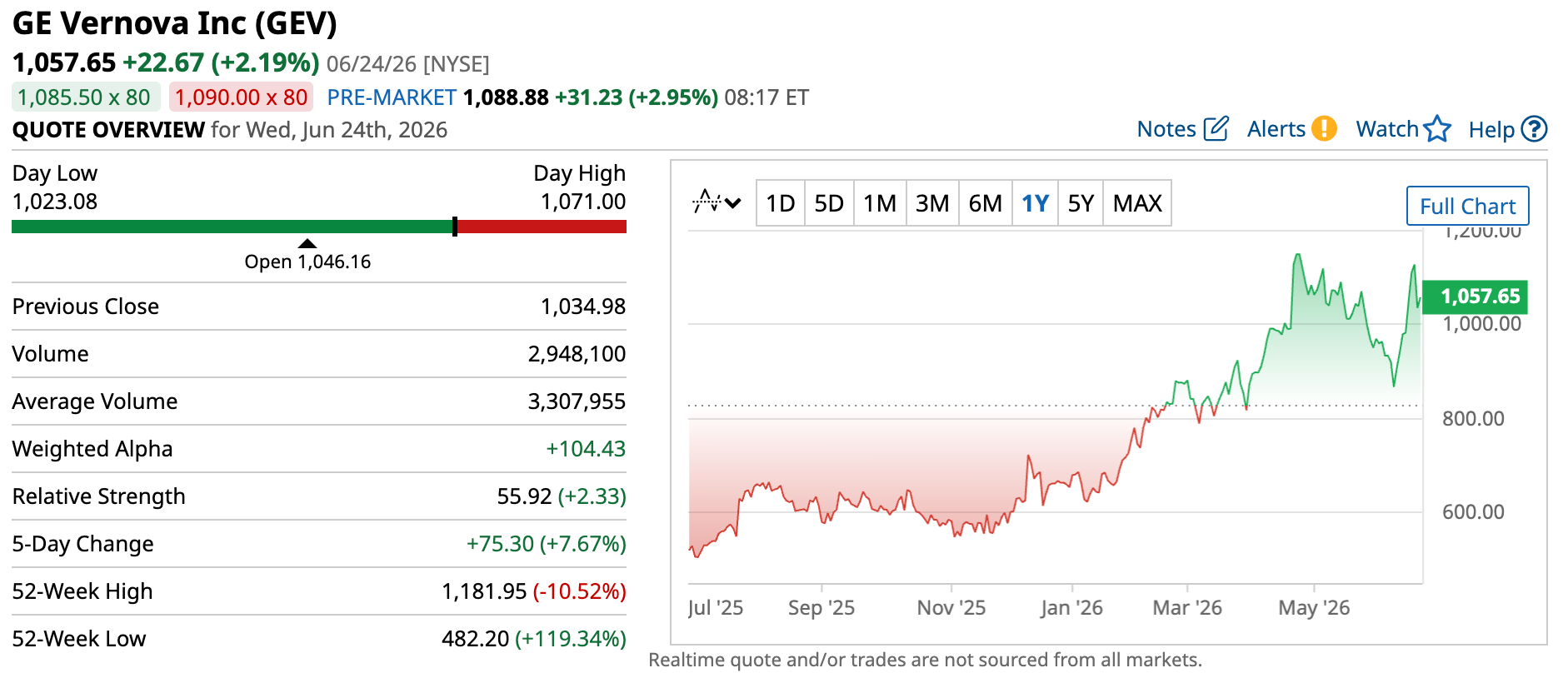

Finally, there’s GE Vernova( GEV), representing a different but equally critical layer: power-generation equipment itself.

GEV is the blue-chip spinoff champ.

GEV is the blue-chip spinoff champ.

GE Vernova makes gas turbines, renewable energy systems, and grid-scale electrification infrastructure. While companies like Constellation and Talen generate electricity, GE Vernova often supplies the equipment that makes it possible.

Increasing AI demand results in more power demand, and if the producers don’t have the existing facilities to cover that demand – well, then, they’re going to need to expand. That means GE Vernova directly benefits from increased AI power requirements. Here are a few examples.

Last year, GE Vernova partnered with Crusoe, a vertically integrated AI infrastructure provider, to deliver 29 new gas turbines to its data centers. This combined deployment is expected to support up to 1 gigawatt of electricity production. They also partnered with Amazon Web Services, Inc. to offer a broad range of energy solutions covering electrification systems, renewables, and power generation services all to support global data center expansion.

And I wouldn’t want to suggest that the client base is limited to hyperscalers. GE Vernova is one of the most dominant and important energy infrastructure players in the world, so naturally, the deals go beyond AI. Companies like Duke Energy ( DUK) and Chevron ( CVX) all have existing deals with GE Vernova. The company is also a key player in national energy expansion initiatives, such as the one in Saudi Arabia, which is estimated to reach up to $14.2 billion over its lifetime.

The risks of investing in AI power stocks

Overall, the AI data center build-out is extremely beneficial to all links of the energy value chain. But there are risks that investors need to grapple with. Some of them aren’t even theoretical; they’re here, and they’re looming. The only thing we don’t know is when exactly they will make landfall.

The first risk is the cycle

The first and arguably the most critical risk is cyclicality. Right now, the world's largest companies are shelling out billions to each support their own AI initiatives. Microsoft, Amazon, Alphabet, and Meta have already committed to increasing their capex explicitly to expand their data centers and other AI infrastructure. They want better LLMs, features, functionality, and narratives for their shareholder presentations.

The race, as they say, is on. But how long will the run last? Because let’s face it: even though it seems like hyperscalers have bottomless wells of money, they will eventually hit bedrock with increasing and sustained AI expenditure. One of these days, they will have to slow down spending. And once they do, power will be one of the cut-off points.

That means less demand for equipment, power generation, infrastructure, system solutions, and all the rest.

By the way, this isn’t me reading tea leaves for the AI power industry. There’s a historical precedent here. Capital-intensive industries have always been cyclical. Cycles may expand for years or even decades, but a downturn is always inevitable. We saw it with telecom, oil and gas, the first nuclear buildout cycle, and other emerging sectors during their times.

Too hot, too cold, never just right

Investors also need to keep an eye on signs of under- and overbuilding. The power sector is notoriously sensitive to such risks, due to the long lead times for buildouts across, well, every link in the value chain.

Turbines, transformers, and nuclear power plants don’t magically appear whenever a hyperscaler wants them to. They could take years to manufacture – even longer if the infrastructure to build them isn’t in place yet – which leads to a nice little two-sided risk for both the manufacturer and the client.

Too much demand and too little infrastructure? Those are underbuilds. The logical fix for that is to expand.

But what if demand fizzles out?

That same expanded infrastructure that was so critical to meet demand a few years before is now sitting idle, collecting dust.

In short, overbuilds.

Two sides of the same coin.

The last risk is concentration

And finally, one of the biggest risks of AI power is in the name itself.

Artificial intelligence.

One sector. One market. One group of customers pay all the bills.

That’s the reality today behind the AI boom. I know it might sound like I’m scratching my nails against a chalkboard by repeating the same few names, but be that it as it may, Microsoft, Amazon, Google, and Meta are among the biggest and most aggressive spenders right now. Every decision they make trickles down the AI value chain, including power.

So, if even one of those tech giants decides to slow down, delay projects, or build their own power solutions, the effects could ripple across the sector. Suddenly, utilities find themselves needing less incremental generation capacity. Fewer data centers would need to be connected to the grid. Equipment orders could slow. Infrastructure projects could be deferred.

The bottom line for AI power stocks

What this ultimately comes down to is a shift in where the constraints sit in the AI ecosystem. The early phase was defined by compute scarcity, and that's when semiconductors took center stage. Then memory became the hot commodity, and RAM manufacturers got their moment in the sun.

But as the buildouts scale, the constraints keep moving downstream, into the physical infrastructure that supports all that compute. Power generation. Transmission. The equipment that makes it all run.

So the next shift in the industry's center of gravity? It's heading straight to power. And that's what makes this so compelling: the companies at these bottlenecks aren't betting on which chatbot wins or whose model tops the leaderboard. They get paid no matter which name comes out on top, because every one of them needs electricity to compete.

But here's the part that should excite long-term investors most. Even when the AI spending cycle eventually cools – and it will – the world doesn't suddenly need less power. Electrification, reshoring, grid modernization, and rising global demand were already pushing this sector higher long before the first hyperscaler signed a PPA. AI didn't create the power supercycle. It simply poured gasoline on the fire (so to speak).

That's the rare setup: a theme with a massive near-term catalyst and a durable, decades-long tailwind underneath it. The bottleneck is real, the demand is here, and the companies that deliver the electricity, systems, and infrastructure to run the AI era are positioned to benefit for years to come.

Just remember that market positions and moats can shift, so stay on top of your picks. But if the center of gravity really is moving to power, the opportunity in front of investors right now is hard to ignore.

On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

Related Symbols

| Symbol | Last | Chg | %Chg |

|---|---|---|---|

| NVDA | 192.53 | -3.21 | -1.64% |

| Nvidia Corp | |||

| GOOGL | 337.39 | -6.32 | -1.84% |

| Alphabet Cl A | |||

| META | 550.25 | +7.38 | +1.36% |

| META Platforms Inc | |||

| AVGO | 365.02 | -13.89 | -3.67% |

| Broadcom Ltd | |||

| CEG | 264.02 | -4.67 | -1.74% |

| Constellation Energy Corp | |||

| PWR | 687.87 | -30.72 | -4.28% |

| Quanta Services | |||

| CCJ | 104.49 | +0.91 | +0.88% |

| Cameco Corp | |||

| NGQ26 | 3.279s | -0.016 | -0.49% |

| Natural Gas | |||

| MSFT | 372.97 | +20.14 | +5.71% |

| Microsoft Corp | |||

| TLN | 404.09 | -12.71 | -3.05% |

| Talen Energy Corporation | |||

| AMD | 521.58 | -10.99 | -2.06% |

| Adv Micro Devices | |||

| GEV | 1,045.17 | -40.30 | -3.71% |

| GE Vernova Inc | |||

| SBGSF | 313.6160 | -9.3840 | -2.91% |

| Schneider Electric Sa | |||

| DUK | 128.40 | +1.29 | +1.01% |

| Duke Energy Corp | |||

| AMZN | 232.69 | +5.68 | +2.50% |

| Amazon.com Inc | |||

| ETN | 402.68 | -17.19 | -4.09% |

| Eaton Corp | |||

| MRVL | 266.77 | -14.49 | -5.15% |

| Marvell Technology Inc |

Most Popular News

1\

\

Peter Thiel Took $1,700 and a Standard Roth IRA Account and Turned It Into $5 Billion. You Can Do It Too.

1\

\

Peter Thiel Took $1,700 and a Standard Roth IRA Account and Turned It Into $5 Billion. You Can Do It Too. 3\

\

Stocks Erase Early Gain as Megacap Tech Stocks Retreat

3\

\

Stocks Erase Early Gain as Megacap Tech Stocks Retreat

4\

\

Stocks Rally Before the Open on Upbeat Micron Earnings, U.S. PCE Inflation Data in Focus

4\

\

Stocks Rally Before the Open on Upbeat Micron Earnings, U.S. PCE Inflation Data in Focus

/A%20close-up%20of%20a%20General%20Motors%20corporate%20sign%20by%20lindaparton%20via%20Adobe%20Stock.jpeg) 5\

\

Scalp a Quick Profit on General Motors Stock with This Contrarian Option Trade

5\

\

Scalp a Quick Profit on General Motors Stock with This Contrarian Option Trade

Want to use this as your default charts setting?

Save this setup as a Chart Templates

Switch the Market flag

for targeted data from your country of choice.

Open the menu and switch the

Market flag for targeted data from your country of choice.

Want Streaming Chart Updates?

Switch your Site Preferences

to use Interactive Charts

Need More Chart Options?

Right-click on the chart to open the Interactive Chart menu.

Use your up/down arrows to move through the symbols.

Read Original at Barchart.com →