Accessibility help Skip to navigation Skip to main content Skip to footer

Add to myFT

Get instant alerts for this topic

Manage your delivery channels here Remove from myFT

The space bit of SpaceX is worth $8 a share, says Morgan Stanley

You miss all the moonshots you don’t take

-

The space bit of SpaceX is worth $8 a share, says Morgan Stanley on x (opens in a new window)

-

The space bit of SpaceX is worth $8 a share, says Morgan Stanley on facebook (opens in a new window)

-

The space bit of SpaceX is worth $8 a share, says Morgan Stanley on linkedin (opens in a new window)

-

The space bit of SpaceX is worth $8 a share, says Morgan Stanley on whatsapp (opens in a new window)

-

Save

-

The space bit of SpaceX is worth $8 a share, says Morgan Stanley on x (opens in a new window)

-

The space bit of SpaceX is worth $8 a share, says Morgan Stanley on facebook (opens in a new window)

-

The space bit of SpaceX is worth $8 a share, says Morgan Stanley on linkedin (opens in a new window)

-

The space bit of SpaceX is worth $8 a share, says Morgan Stanley on whatsapp (opens in a new window)

-

Save

PublishedJuly 7 2026

Jump to comments section Print this page

Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

SpaceX and Adam Jonas! It’s a dream collaboration, where “dream” can mean any of these . . .

Here’s paragraph one of the Morgan Stanley’s SpaceX initiation note:

With an ‘X of 1’ position in space infrastructure, we believe SpaceX can convert energy into intelligence at scale with optionality to monetize through a range of consumer and enterprise solutions for the next era of AI… the final frontier.

Jonas — formerly the Wall Street bank’s Tesla and occasionally other auto companies analyst — was last year reallocated to the sort of free-radical futurologist role we’d thought had been cornered by Shingy.

The SpaceX float gave second billing to Morgan Stanley, potentially for reasons alphabetical. So, with the research blackout for SpaceX’s main bookrunners now lifted, Jonas can be frontman to MS’s team of eight as they seek to explain to clients why a $2tn telecoms operator and government engineering contractor is a good purchase on fundamentals all the way up to 567 times forward earnings:

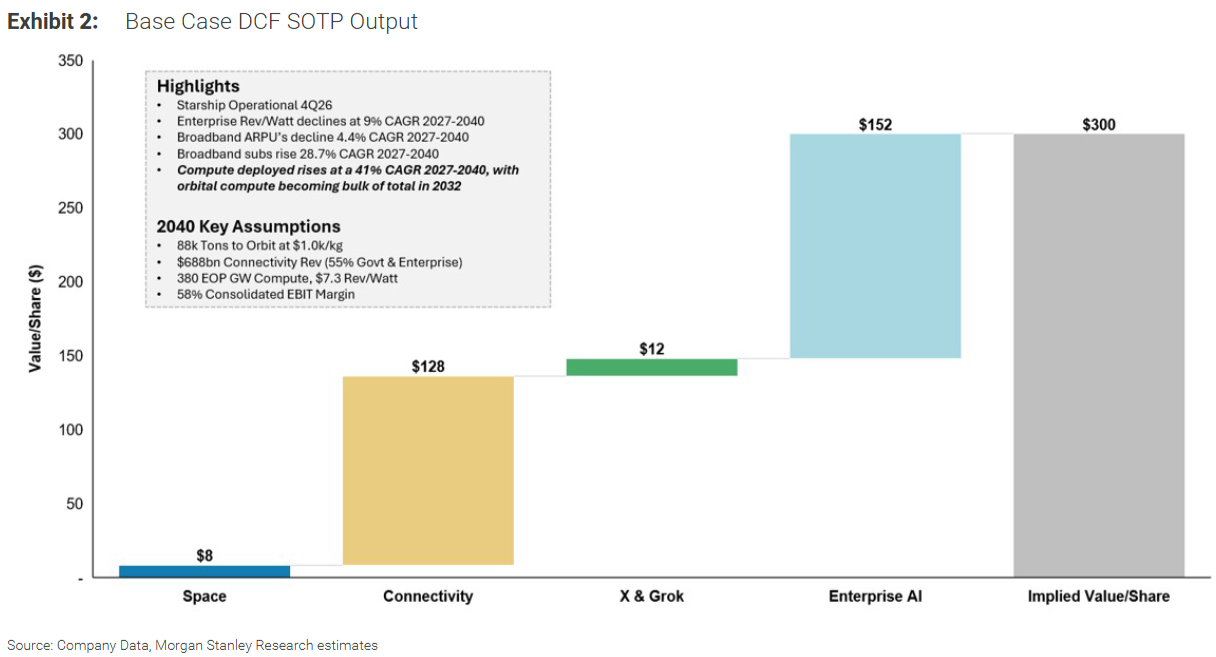

We initiate coverage of SpaceX at Overweight with a $300 price target. SpaceX combines near-monopoly launch economics, the world’s largest LEO satellite network, and a fast-scaling AI infrastructure business. We see the company as one of the few platforms that can link real estate in orbit, global connectivity, and compute capacity into one infrastructure stack. Our base case models revenue rising from $45bn in 2026 to $319bn in 2030 and $3.3tn in 2040, with the largest upside tied to Starship, Starlink capacity, terrestrial compute, and orbital compute.

[ Big]

{kind=link}

Too complicated, AJ. Explain it to me like I’m five:

Not five months . . .

Better! Though maybe, as an investment case, “AI informs infrastructure improvements” feels a little woollier than “space enables satellite network”. Space demonstrably exists. Things that don’t exist yet include fully reusable rockets, orbital data centres, pocketable high-bandwidth satellite phones and profit from operating large language models at scale. That doesn’t mean they never will; it just means we might want to incorporate a bit of caution around the timelines for development and commercial adoption.

Or not!

[ Big]

{kind=link}

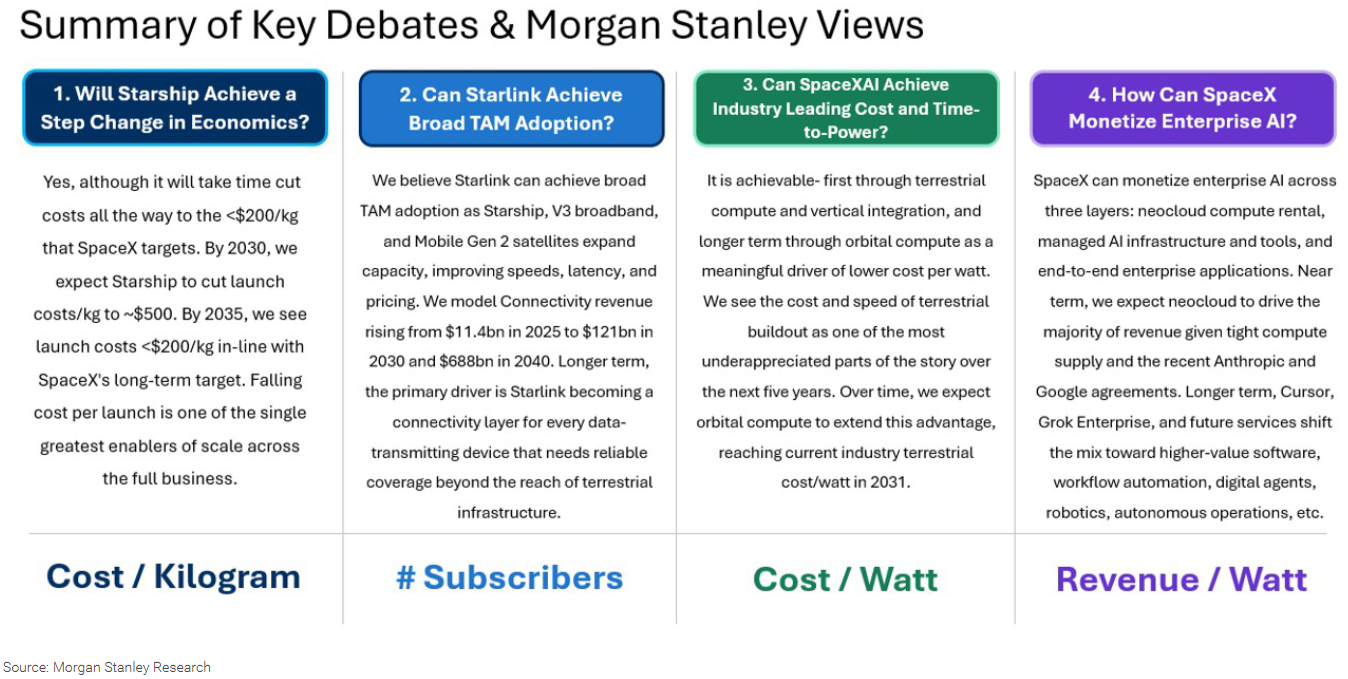

Starting with the reusable rockets, MS expects SpaceX to eat itself. Launch costs will collapse by more than 99 per cent versus their historical average within 10 years, it says. Operating margin on launches will have jumped to about 40 per cent, from around negative 50 per cent currently, but 40 per cent of less than 1 per cent still isn’t very much.

That’s why the Space bit of SpaceX provides just 3 per cent of MS’s base-case valuation. “The segment is largely treated as a cost centre for the broader company rather than a standalone launch-maximisation business,” say Jonas et al.

For Starlink, MS forecasts an impressively precise $687.7bn in revenue for 2040. Last year it did $11.4bn.

Longer term, there’s a whole world out there of redundant connectivity. “[T]he primary driver is Starlink becoming a connectivity layer for every data-transmitting device that needs reliable coverage beyond the reach of terrestrial infrastructure,” it says.

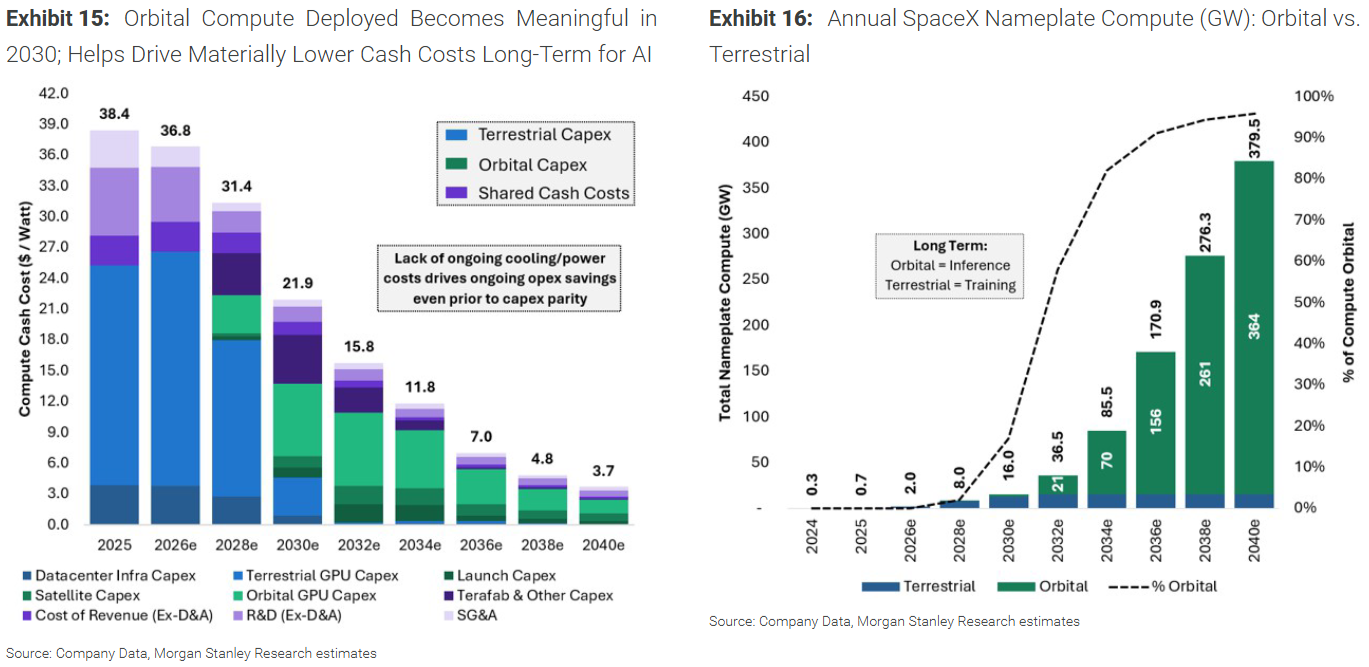

The other half of the MS model is data centres. “Orbital compute deployments” start in 2028, reach cost parity with their earthbound equivalents by 2031, and put 364GW of rigs in space by 2040. To put that figure in some kind of context, it’s about 40GW shy of the global operating nuclear capacity:

[ Big]

{kind=link}

Finally, Grok:

Enterprise AI is the largest opportunity in our model, with SpaceX able to monetize across three layers: neocloud compute rental, managed AI infrastructure, and full enterprise applications. We model AI revenue rising from approximately $22bn in 2026 to $190bn in 2030 and $2.6tn in 2040, with Enterprise AI representing the majority of the segment over time. Near term, we expect neocloud to drive most revenue given tight compute supply and recent Anthropic (disclosed in S-1), Google (signed early June), and the reported Reflection (not confirmed by company) agreements, which we estimate represent roughly $28bn of annualized revenue runrate through 2029.

Longer term, we expect SpaceX to push beyond raw compute rental into higher-value software and workflow automation. Cursor, Grok Enterprise, Macrohard, and agentic AI tools could help shift revenue toward coding, digital agents, robotics, autonomous operations, enterprise workflows, and other AI-enabled services.

Sounds expensive! But, SpaceX having raised $85.7bn with a(n underwhelming) share sale and $25bn with a ( badly received) bond issue, it has to be too soon to be talking about fundraisings.

Or not!

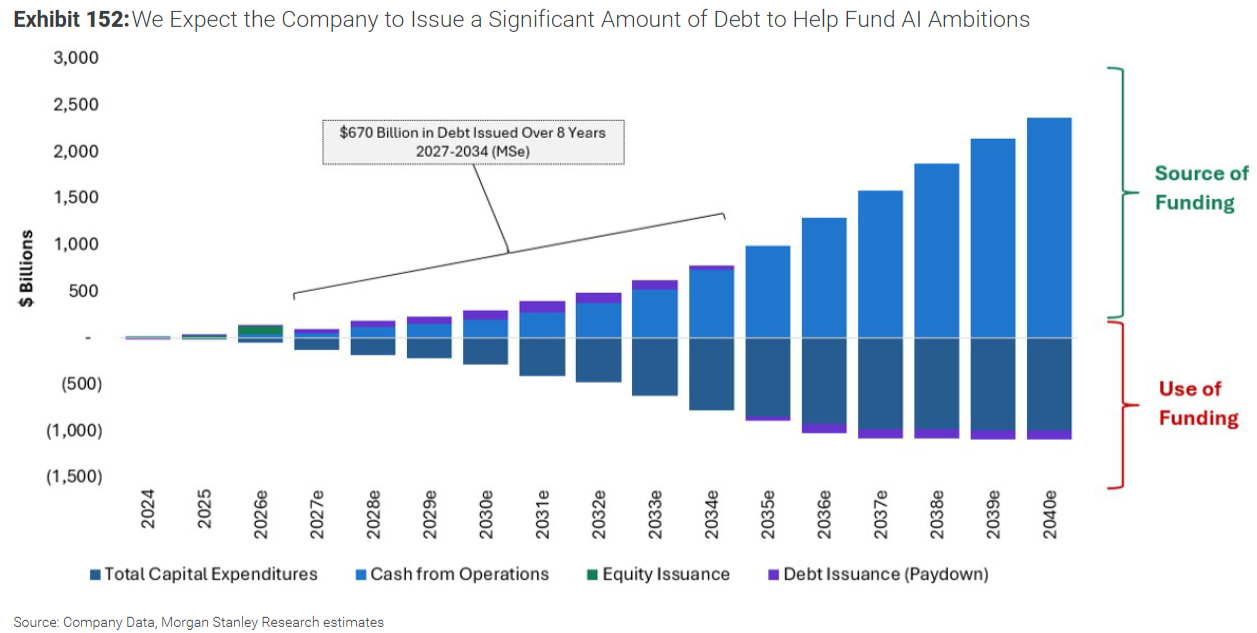

We currently model the company funding growth through non-convertible debt, but future equity dilution remains a material risk if debt markets cannot absorb SpaceX’s financing needs or if credit rating agencies conclude that additional leverage would pressure the company’s credit profile. In that scenario, SpaceX may need to issue equity, reduce growth investment, or slow its deployment plans. We would also note that SpaceX included the following blurb in an amendment to its S-1: “We may issue a significant amount of equity in connection with future transactions.”

In our model, we estimate SpaceX raising an average of $72bn annually between 2027 and 2030 and then an average of $95bn annually between 2031 and 2034. However, note that the mix of funding shifts dramatically towards cash from operations vs. debt financing over this time horizon and gross leverage / EBITDA stays well under 2x in all forecast years.

[ Big]

{kind=link}

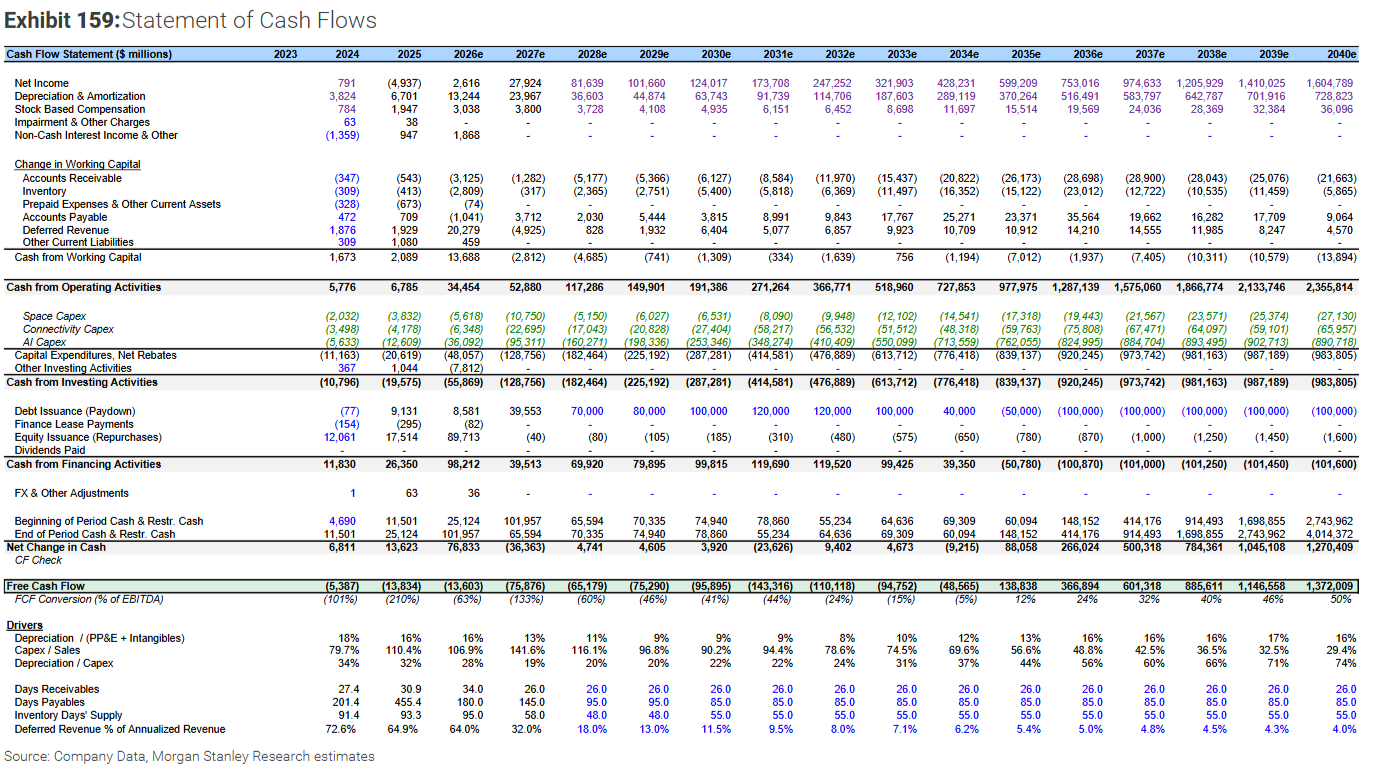

A $668bn funding obligation to 2034 that delivers free cash flow that year of negative $48bn sounds less than ideal, though FCF might flip positive to $138bn in 2035 if everything goes to plan, so that’s nice. The SpaceX CEO presumably has a long history of delivering products on time and to the required specification that can support such confidence.

Given how little extant business there is to work with, the team has been inventive in how it back-engineers a headline valuation. At $300 per share the Space and Connectivity side of SpaceX would be valued on par with Tesla while the rest gets a Palantir valuation, and at 56 times 2028 EV/Ebitda and 21 times EV/sales, respectively.

For any investor who prefers wholeco to sum-of-the-parts, MS suggests the rarely used EV/Ebit/growth ratio. Pricing SpaceX at $300 translates to 0.41 times 2028 EV/Ebit/growth, which places the stock below the 25th percentile of peers — the peers being any other big company that’s similarly hope and hype:

Forecasts are the last thing anyone pays attention to in a Jonas note, however. Working through this one, it becomes fairly easy to spot which of its authors wrote which bit.

For example:

Why go to the Moon?

The Moon is not the end goal for SpaceX, but it could become the most practical near-term platform for learning how to live, build, and manufacture away from Earth. The Moon is roughly three days from Earth versus months to Mars, has more frequent launch windows, and offers a lower-gravity environment that could make surface-to-space logistics easier over time. In our view, the lunar opportunity is best seen as a call option on future space infrastructure rather than a near-term revenue driver.

[..,]

And shortly after that . . .

Helium-3: The Moon’s most strategically important resource?

Helium-3 is one of the clearest examples of why lunar infrastructure could matter. The isotope is extremely rare on Earth, with current supply largely tied to tritium decay, but the Moon has accumulated helium-3 for billions of years because it lacks Earth’s atmosphere and magnetic field. NASA mining concepts often assume concentrations around 20 parts per billion, meaning helium-3 is abundant in total but painfully diffuse, requiring hundreds of tons of regolith to be mined and heated to recover small quantities. For quantum, helium-3 is important because dilution refrigerators use helium-3 and helium-4 mixtures to cool quantum processors to millikelvin temperatures, reducing thermal noise and helping preserve fragile qubit states. For fusion, helium-3 is attractive because deuterium-helium-3 reactions could generate charged particles instead of most neutron output, potentially reducing radiation damage, shielding needs, and longlived radioactive waste versus deuterium-tritium fusion.

Awesome! Also, did we mention the $600 bull case?

[ Big]

{kind=link}

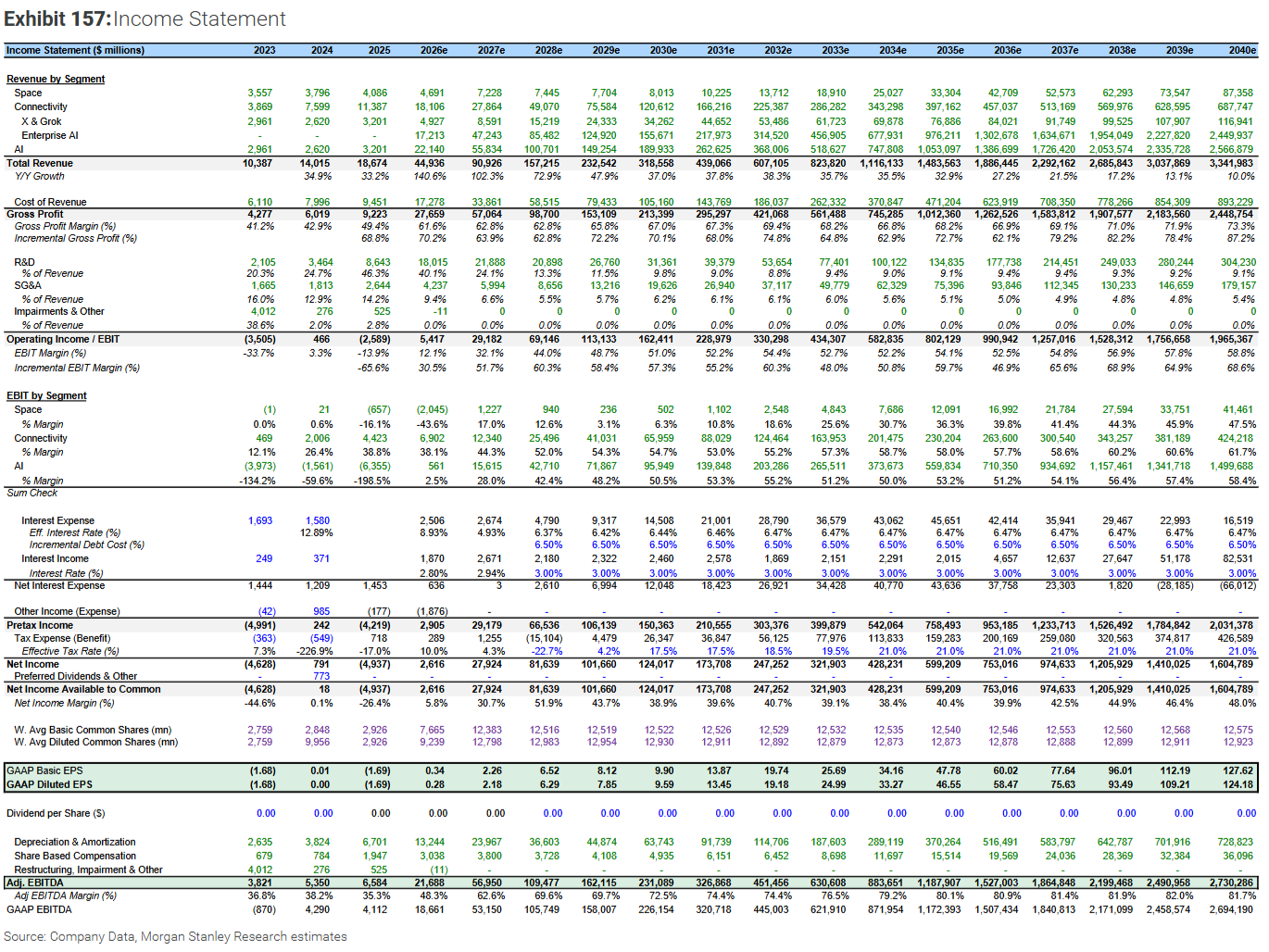

For posterity if nothing else, we’ve screenshotted the MS forecast tables for income and cash flow. And in case you’re wondering, at no point in the initiation note’s 141 pages does Jonas explain what “an ‘X of 1’ position in space infrastructure” actually means.

{kind=link}

{kind=link}

Further reading

— Tesla, magical thinking, and the madness of obsession

— SpaceX: the final frontier of IPOs

Reuse this content(opens in new window) CommentsJump to comments section

Follow the topics in this article

Add to myFT

Add to myFT

Add to myFT

Add to myFT

Add to myFT

Comments

Close side navigation menu

Search the FTSearch

Read Original at Financial Times →