Main Menu

U.S. Edition

Follow Us

Follow us on facebookFollow us on xFollow us on instagram

Part of HuffPost News. ©2026 BuzzFeed, Inc. All rights reserved.

×

Loading comments...

What's Hot

Fund TheFirstAmendment

The First Amendment protects a free press. It doesn't fund one. HuffPost members help make independent journalism possible. Join today.

Already a member? Log in to hide these messages.

LOADINGERROR LOADING

The official launch of Trump Accounts for children this week has sparked skepticism and hesitancy from some parents, with concerns that the free investment program could be a scam, bogus, or later used against them.

“The amount of grift from this administration is off the charts, so I’m hesitant to trust any funds they establish,” one parent told HuffPost.

Advertisement

“Take a second and think about literally any other deal Trump has made with anyone. How’d that work out?” another person wrote in an online forum discussing the program’s legitimacy.

Mississippi Sen. Bennie Thompson (D) also dismissed the program, telling his constituents on Monday that he personally “would pass” on opening an account. Thompson, 78, has one adult daughter, according to his website, who wouldn’t qualify for one.

It's safe to say, I would pass on a Trump account.

Trump University already taught us what happens when his name is on the brochure. Does a $25 million settlement ring a bell? https://t.co/ubClyrPPbq

— Rep. Bennie G. Thompson (@BennieGThompson) July 6, 2026

Advertisement

“Trump University already taught us what happens when his name is on the brochure,” stated Thompson, likening the accounts to Trump’s failed university.

A spokesperson for Thompson’s office told HuffPost that his point was that federal aid should go toward strengthening existing programs, like Social Security and food stamps. The Joint Committee on Taxation has estimated that Trump accounts will cost the federal government around $15 billion through 2034.

While the accounts may raise concerns and red flags for some, financial advisors have encouraged parents and guardians to take the money and have compared the accounts with other established IRA investment accounts for minors. They’re also set up through the U.S. Treasury Department, which they say offers government security for those skeptical of its legitimacy.

Advertisement

“I think there’s always going to be hesitancy when something comes around like this,” Johnson Rhett, a certified financial advisor with Branning Wealth Management, told HuffPost on Wednesday. Rhett, whose firm offers fee-only fiduciary advice, said he’s received calls from people asking how to get the “free money” and whether it’s “too good to be true.”

Many financial advisors have argued that better savings programs exist over President Donald Trump's free investment program called Trump Accounts. But parents are still advised to register to take advantage of the $1,000 seed money.

via Associated Press

“It is technically through the Treasury, which gives me, as a planner, some solace,” he said. “You’re talking about an official government website. Now it’s a completely other thing if someone says, ‘Hey, I don’t necessarily trust the government.’ But there is some safeguard with it being through that.”

Advertisement

As the current pilot program boasts, each qualifying applicant born between 2025 and 2028 would receive $1,000 in government seed money, which would be invested by default into a U.S. stock fund. The money can be left untouched and allowed to grow, or more can be added ― though many financial advisors suggest diversifying and utilizing investment accounts like 529 plans or brokerage accounts instead, arguing they have better tax advantages.

Rhett advises having a Trump Account along with a 529 account for tax-free education savings, and a Roth IRA if the child has earned income. “Don’t treat this as your only savings strategy for your child,” he advises in an online financial planning guide.

Parents or legal guardians also don’t need to download the Trump Accounts app to apply. IRS Form 4547 can be submitted through the IRS’s website, which the IRS estimates takes 5 to 10 minutes.

Advertisement

A screen displays information about Trump Accounts on the floor at the New York Stock Exchange in New York on July 6.

via Associated Press

“I did end up opening accounts for [my children] through the IRS portal as I was more comfortable using a platform that is (at least somewhat) bound by government rules and laws regarding data protection,” one parent told HuffPost, after initial hesitancy to sign up.

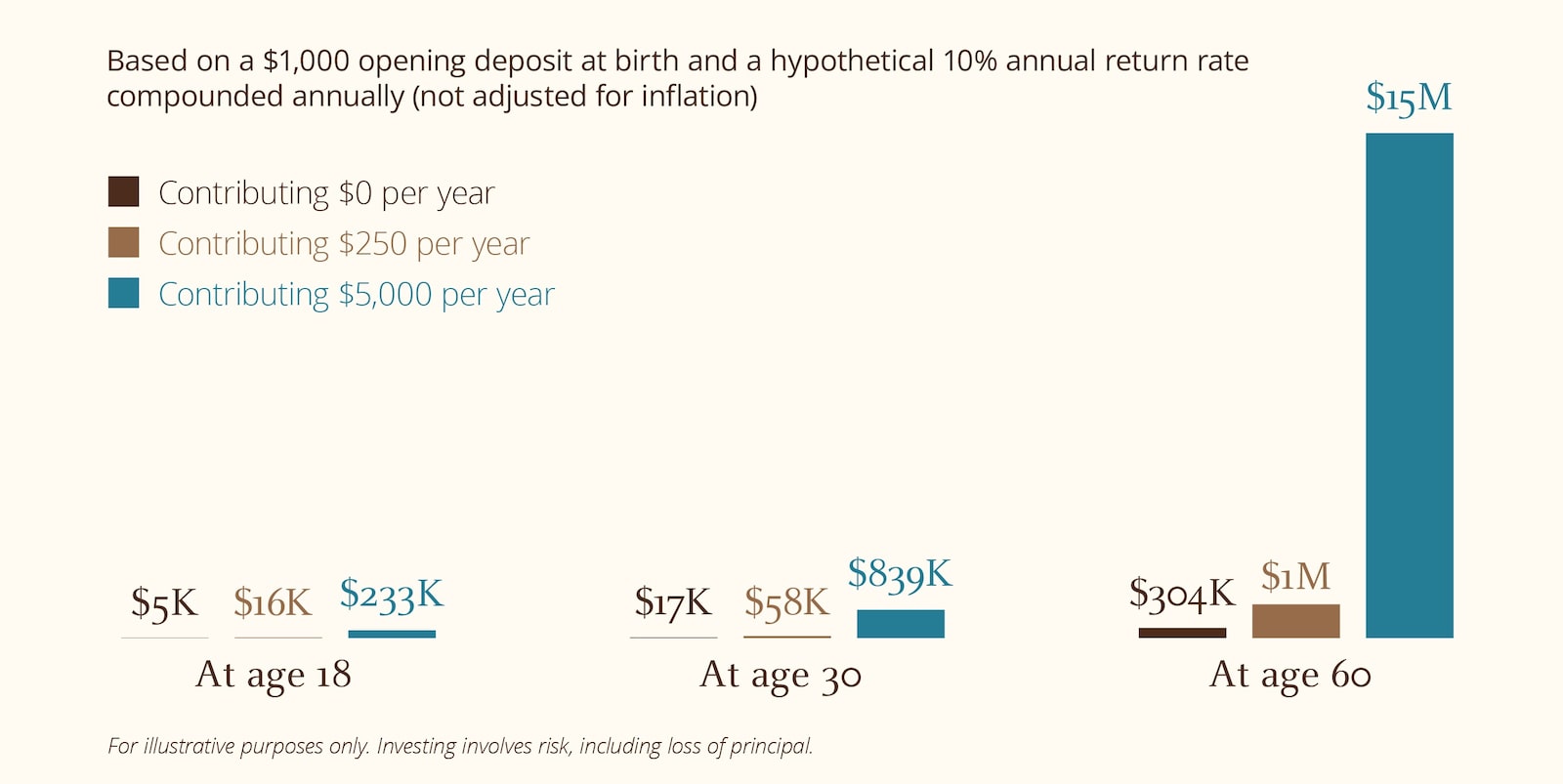

By the time the child is 18, an untouched account ― meaning no additional contributions ― could total around $5,000, according to one estimate by J.P. Morgan. Contributing an additional $250 per year to the account could raise it to $16,000 within that same time.

{kind=link}

Advertisement

“For eligible families, there doesn’t seem to be a financial downside to getting the $1,000 government funding, even if no other money is added to the account,” Adam Frank, head of wealth planning and advice at J.P. Morgan Wealth Management, said in an online explainer.

In addition to the government’s one-time $1,000 deposit, there are options for free additional contributions from elsewhere.

The Dell Foundation, for example, has agreed to donate $250 to the accounts of children aged 10 and under who live in zip codes where the median income is $150,000 or less, up to $6.25 billion. Children in Connecticut are similarly eligible for an additional $250 thanks to a donation by Dalio Philanthropies.

Advertisement

Once the account holder turns 18, the account unlocks and converts to a tax-deferred Traditional IRA. Money can be withdrawn without a 10% penalty for certain approved purposes — such as education and first-time home buying ― or it can be left to grow. The 10% penalty is lifted once the account holder turns 59 1/2, according to the Congressional Research Service.

“You could take the $1,000 upfront from the government … let it grow until the child is 18 and then do what you want with it,” said Rhett of those not wanting to personally contribute. “You’re not going to have to pay taxes on it each year, by any means. It’s similar to a traditional IRA where, unless you’re taking the money out of the account, it’s tax-deferred; there’s no tax consequence in that tax year.”

While it’s up to parents or legal guardians to decide on whether to sign their child up, Rhett advises reaching out to a financial advisor to determine the best savings goals and strategies for their child.

Advertisement

“I understand that [Trump] is a very polarizing figure and I think that’s some of the hold up for people willing to open up the accounts and accept the $1,000, and again that’s completely up to them,” he said. “You need to do your own due diligence or talk with your advisor about it, or some combination of both.”

Leave a Comment

Share on facebook Email this article

Suggest a correction

|

Advertisement

From Our Partner

Close

Trending In U.S. News

More In U.S. News

Read Original at HuffPost →